INTRODUCTION

Money mistakes in your 30s can shape your entire financial future. This decade is a powerful turning point: your career is growing, you might be starting a family, buying a home, or making big lifestyle choices. But with these new opportunities come bigger responsibilities and bigger risks if you make the wrong moves.

Many people in their 30s feel pressure to “keep up” with friends or social media, leading to overspending and debt. Others put off saving for retirement, thinking they have plenty of time.

If you don’t pay attention now, these mistakes can lead to years of stress, missed opportunities, and financial setbacks. The good news is, you can avoid these pitfalls with the right knowledge and habits. Let’s dive into the most common money mistakes to avoid in your 30s and see how real people have learned from their experiences.

Money Mistakes to Avoid in Your 30s

Your 30s are a time of major life changes and financial decisions. Here are the top money mistakes to avoid in your 30s:

1. Living Beyond Your Means

Spending more than you earn is a common money mistake in your 30s. Lifestyle inflation—upgrading your home, car, or vacations as your income rises—can leave you with little savings for emergencies or investments.

2. Overspending on Housing

Many people stretch their budgets to buy or rent homes they can’t truly afford. This can cause financial stress and limit your ability to save or invest for the future.

3. Buying an Expensive Car

New cars lose value quickly. Buying a car that’s too expensive, especially with borrowed money, means you’re paying interest on something that drops in value every year.

4. Relying Too Much on Credit Cards

Using credit cards for daily expenses and not paying off the full balance each month can lead to high-interest debt that’s hard to escape from.

5. Not Building an Emergency Fund

Life is unpredictable. Without an emergency fund, you might be forced to take out high-interest loans or use credit cards for unexpected expenses. Experts recommend saving at least three to six months of living costs.

6. Delaying Retirement Savings

Thinking retirement is far away is a big money mistake in your 30s. The earlier you start, the more you benefit from compound interest. Even small monthly contributions can grow significantly over time.

7. Ignoring Investments

Simply saving money isn’t enough. Inflation reduces the value of cash over time. Investing in stocks, mutual funds, or retirement accounts helps your money grow faster.

8. Not Having Proper Insurance

Skipping health, life, or income protection insurance is risky. Unexpected illness, accidents, or death can leave you and your family in financial trouble. Make sure you have adequate coverage.

9. Failing to Make a Will or Estate Plan

Many people in their 30s feel “bulletproof” and put off creating a will or estate plan. But accidents and illness can happen at any age. Having a will and powers of attorney protects your loved ones and your assets.

10. Not Tracking Your Spending and Budgeting

Operating without a clear budget makes it easy to overspend and under-save. Review and update your budget regularly to reflect changes in your income and expenses.

Five Real-Life Case Studies

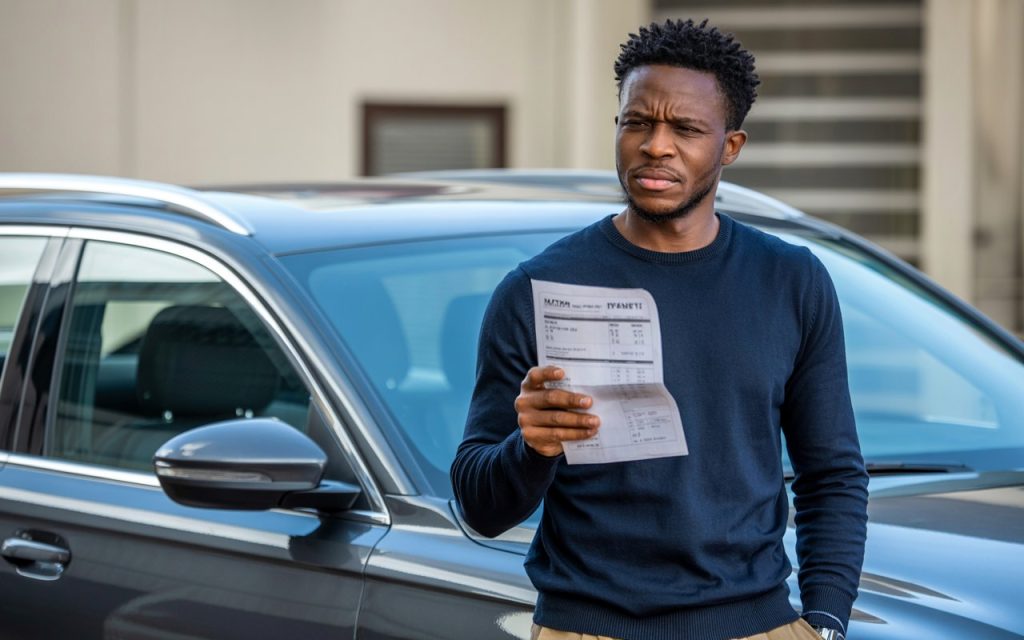

- Ayo’s Story: At 32, Ayo bought a brand-new car with a big loan, thinking it would boost his image and make commuting easier. But the monthly payments and high insurance costs quickly ate up half his salary. He soon realized he had no money left for savings or emergencies. Looking back, Ayo wishes he had bought a used car within his budget and saved the difference.

2. Chidi’s Experience: Chidi, 35, wanted to enjoy life and travel like his friends. He used his credit card to fund several vacations, believing he could pay it off later. The debt piled up, and the interest charges became overwhelming. Chidi learned the hard way that using credit for luxury expenses can lead to long-term financial stress.

3. Ngozi’s Lesson: Ngozi, 31, always thought retirement was too far away to worry about. She focused on paying bills and enjoying her present lifestyle, putting off any retirement savings. Years later, she realized she had missed out on valuable time for her money to grow through compound interest. Now, she encourages others to start saving for retirement early, even with small amounts.

4. Bola’s Challenge: At 38, Bola lost her job unexpectedly. She had no emergency fund and had to borrow from friends and family just to pay her rent and buy food. This experience taught her the importance of having a financial safety net to cover at least three to six months of living expenses.

5. Tunde’s Wake-Up Call: Tunde, 34, ignored health insurance because he felt healthy and wanted to save money. After a sudden accident, he faced huge medical bills that wiped out his savings. Tunde now understands that insurance is not just an expense—it’s essential protection for your future.

Smart Alternatives to Common Money Mistakes in Your 30s

Here are practical steps you can take instead of making these common mistakes:

| Money Mistake | Smart Alternative |

|---|---|

| Living beyond your means | Create and stick to a realistic budget |

| Overspending on housing | Choose a home you can comfortably afford |

| Buying an expensive car | Buy a reliable used car or lease wisely |

| Relying too much on credit cards | Use cash or debit and pay off balances |

| Not building an emergency fund | Save a little each month in a separate account |

| Delaying retirement savings | Start with small, regular contributions |

| Ignoring investments | Invest in low-cost funds or retirement plans |

| Not having proper insurance | Get basic health and life insurance |

| Failing to make a will or estate plan | Write a simple will and update as needed |

| Not tracking spending and budgeting | Use budgeting apps or spreadsheets |

Money Mistakes to Avoid in Your 30s: Powerful Habits for Success

- Practice conscious spending by focusing on needs over wants and saving extra income before increasing your lifestyle

- Automate your savings and investments with regular transfers to your accounts

- Pay off high-interest debt as quickly as possible to avoid losing money to interest

- Review your insurance coverage every year to make sure you and your family are protected

- Build and maintain good credit by paying bills on time and keeping credit balances low

- Diversify your investments to reduce risk and grow your wealth over time

Quotes

- “Money mistakes in your 30s can shape your entire financial future.”

- “If you don’t pay attention now, these mistakes can lead to years of stress, missed opportunities, and financial setbacks.”

- “The good news is, you can avoid these pitfalls with the right knowledge and habits.”

- “Start saving for retirement early, even with small amounts.”

- “Insurance is not just an expense—it’s essential protection for your future.”

- “Avoiding these money mistakes in your 30s will help you build a strong financial foundation and enjoy greater freedom in the future.”

Highlighted Points

- Your 30s are a powerful turning point for your finances—small mistakes now can have big consequences later.

- Living beyond your means and overspending on housing are two of the most common traps.

- Not building an emergency fund leaves you vulnerable to unexpected expenses and debt.

- Delaying retirement savings means missing out on the power of compound interest.

- Ignoring investments causes your money to lose value over time due to inflation.

- Proper insurance protects you and your family from financial disaster.

- Failing to make a will or estate plan can create legal and financial problems for your loved ones.

- Tracking your spending and budgeting is the foundation of good money management.

- Smart alternatives: Create a realistic budget, buy only what you can afford, automate savings, and review your financial plan regularly.

- Real-life stories show that learning from others’ mistakes can help you avoid the same pitfalls.

Frequently Asked Questions

Q: How much should I save for emergencies

A: Aim for three to six months of living expenses in a separate, easy-to-access account

Q: Is it too late to start investing in my 30s

A: Not at all. The sooner you start, the better, but your 30s are still a great time to begin investing for long-term growth

Q: What type of insurance do I really need

A: At minimum, health, life, and disability insurance are essential to protect your income and family

Q: Should I update my budget as my income changes

A: Yes. Your budget should reflect your current income and expenses. If you get a raise or take on new expenses, update your budget to ensure you’re still living within your means and saving enough for your goals.

Q: How can I manage debt effectively in my 30s

A: Focus on paying off high-interest debts first, such as credit cards. Some people find it motivating to pay off smaller debts first for a psychological boost, but always make at least the minimum payments on all debts to avoid penalties.

Q: What if I am single and don’t have kids—do I still need a will or insurance

A: Yes. Even if you are single, you should still have a basic will and consider disability or life insurance to protect your assets and your loved ones in case of unexpected events.

Q: How do I avoid lifestyle inflation as my income grows

A: When you get a raise or new income, consider increasing your savings or investments instead of raising your spending. This helps you build wealth faster and avoid living paycheck to paycheck.

Q: Why is following a budget so important in your 30s

A: A budget helps you track your spending, avoid debt, and plan for future goals. Without a budget, it’s easy to overspend and miss out on saving for important milestones like a home, children’s education, or retirement.

Q: Should I get caught up in investment fads

A: No. Stick to investments you understand and diversify your portfolio to reduce risk. Avoid chasing trends that promise quick returns, as these can often lead to losses.

Q: How often should I review my financial plan

A: Review your financial plan at least once a year or whenever you experience a major life change, such as a new job, marriage, or having children. This ensures your plan stays current and effective for your needs.

CONCLUSION

Avoiding these money mistakes in your 30s will help you build a strong financial foundation and enjoy greater freedom in the future. Make smart choices now and your future self will thank you